Navigating Identity Verification and Customer Due Diligence in Banking

Prelude

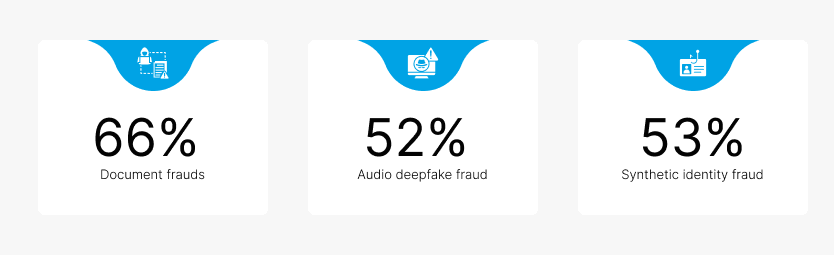

A shocking report about deepfakes exposed the surge in identity fraud in financial sectors.

The report suggests that identity verification is the ultimate solution for shielding organisations from identity theft and financial fraud. Identity verification is the first step of the customer due diligence, which is paramount in customer onboarding in financial services.

This blog discusses the crucial importance of Identity Verification and Customer Due Diligence in Banking.

Identity Verification (IDV) in Customer Due Diligence (CDD)

While customer due diligence serves as a crucial process in assessing risk and ensuring compliance with Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) laws, IDV acts as the first and foundational step in that process. IDV analyses and authenticates the customer’s information to verify its authenticity.

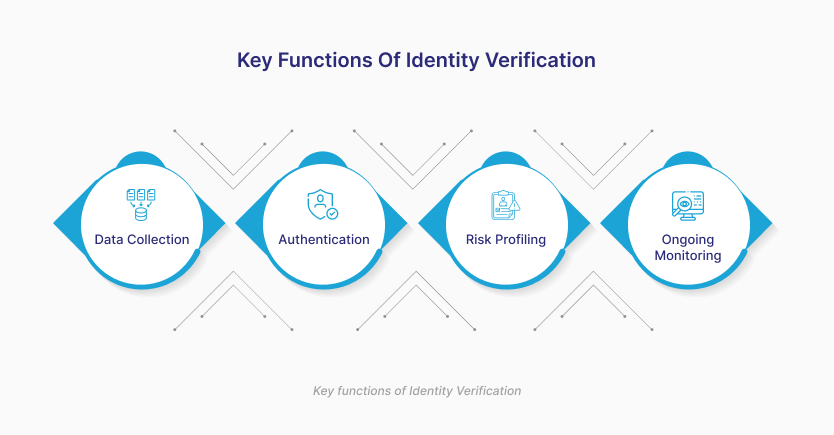

Key functions of Identity Verification:

- Data Collection: During the time of onboarding, IDV collects customers’ sensitive data like ID documents, selfies, biometrics, etc.

- Authentication: Validates the customers’ information by comparing it with the government databases, MRZ (Machine-Readable Zone), or third-party KYC providers.

- Risk Profiling: Using the analyzed data on the customer’s background, geography, profession, and transaction history, customer risk (Politically Exposed Person (PEP), sanctions, watchlists, etc.) is evaluated.

- Ongoing Monitoring: With the risk profile and transaction tracking, the account and the customer’s behaviour are monitored to enable continuous due diligence (e.g., unusual transaction alerts).

High-risk sectors such as finance and banking adopt customer due diligence to shield against fraud (fake documents, identity theft, or synthetic identity) and ensure compliance with global directives, including the FATF, GDPR, and local regulatory frameworks (e.g., SAMA, RBI, or MAS).

The Critical Role of Identity Verification and CDD in Modern Banking

Preventing Financial Fraud

- Challenge: Financial institutions face rising threats from account takeovers, identity theft, phishing scams, and mule account networks. Traditional KYC often fails to detect impersonation or fraudulent documents in real time.

- Solution: Advanced IDV uses biometric facial recognition, liveness detection, and AI-powered document validation to authenticate identities instantly. CDD evaluates customer behaviour and transactional patterns to detect anomalies.

- Process: By verifying both the authenticity of the person and monitoring post-onboarding activities, banks can flag high-risk accounts early and prevent misuse.

- Benefit: Dramatically reduces fraud incidents, improves investigation timelines, and builds long-term system integrity.

Ensuring Regulatory Compliance

- Challenge: Regulatory frameworks like FATF, GDPR, SAMA, and local AML laws require banks to verify identities, monitor accounts, and maintain audit trails. Manual compliance checks are error-prone and resource-intensive.

- Solution: IDV tools automate verification with timestamped records and audit logs. CDD builds risk profiles and maintains ongoing monitoring protocols.

- Process: Real-time compliance checks and risk scoring allow banks to meet evolving regulatory obligations without human bottlenecks.

- Benefit: Avoids penalties, enables scalability, and ensures real-time reporting for internal and external audits.

Strengthening Stakeholder Trust and Supporting Business Growth

- Challenge: Stakeholders, including regulators, partners, and customers, demand transparency and ethical operations, especially in cross-border environments where due diligence expectations vary.

- Solution: IDV validates the true identity of each customer at the point of entry. CDD continuously assesses customer legitimacy based on dynamic data inputs.

- Process: Offers a defensible compliance trail and shows proactive risk governance across all onboarding channels.

- Benefit: Builds institutional credibility, attracts global partnerships, and opens new market segments by demonstrating strong compliance and fraud controls.

Enhancing Risk Management and Streamlining Onboarding

- Challenge: Traditional onboarding is time-consuming, inconsistent, and prone to risk misclassification, resulting in a poor user experience or onboarding of risky users.

- Solution: Automated IDV verifies identity within seconds using OCR, biometrics, and document fraud detection. Risk-based CDD assigns scores and adapts the onboarding flow accordingly.

- Process: Streamlines onboarding while segmenting customers into low/medium/high-risk categories with minimal manual intervention.

- Benefit: Faster onboarding, reduced operational workload, and more accurate risk management from day one.

Enabling Data-Driven Decision-Making

- Challenge: Banks lack granular visibility into customer behaviour, especially post-onboarding, which limits proactive fraud detection and personalised service delivery.

- Solution: CDD frameworks capture transactional data, behavioural biometrics, and KYC refresh intervals, feeding into analytics engines.

- Process: Enables banks to forecast fraud trends, monitor customer lifecycle risks, and derive intelligence for strategic decisions.

- Benefit: Enhances predictive modelling, supports real-time interventions, and improves customer segmentation strategies.

Boosting Operational Efficiency

- Challenge: Manual verification is resource-intensive, slow, and error-prone, leading to long turnaround times and customer drop-offs.

- Solution: AI-driven IDV automates document authentication, face match, and database checks. CDD automation includes dynamic risk scoring and watchlist screening.

- Process: Reduces human intervention, ensures compliance accuracy, and supports 24×7 onboarding without downtime.

- Benefit: Cuts operational costs, reduces average handling time (AHT), and improves customer satisfaction metrics.

Safeguarding Against Synthetic Identities and Deepfakes

- Challenge: Attackers now use AI to create hyper-realistic fake identities and documents that bypass static verification systems.

- Solution: Modern IDV solutions employ liveness detection, 3D facial recognition, and device fingerprinting to distinguish real from synthetic users.

- Process: Identifies fake profiles during onboarding and flags anomalies during ongoing interactions via behavioural analysis.

- Benefit: Reduces exposure to reputational damage and financial losses caused by undetected synthetic fraud.

Supporting Cross-Border Banking Compliance

- Challenge: Global banks must comply with diverse jurisdictional rules, requiring different KYC/AML practices and ID formats, causing friction.

- Solution: IDV solutions integrate with multiple ID databases (e.g., Iqama, Aadhaar, GCC IDs) and support multilingual OCR. CDD adapts risk thresholds by geography.

- Process: Enables seamless onboarding across borders while ensuring local compliance with relevant legal standards.

- Benefit: Promotes international scalability and protects institutions from cross-border regulatory penalties.

Building a Resilient Digital Banking Ecosystem

- Pain Point: Digital banking ecosystems face constant threats, including bot attacks, fraud rings, regulatory changes, and service disruptions.

- Solution: An end-to-end system of identity intelligence, continuous customer due diligence, and automated compliance forms a secure digital foundation.

- Process: Maintains real-time verification, adaptive risk control, and compliance agility in a single operational stack.

- Benefit: Ensures long-term stability, security, and trust in a fully digital environment.

SquareOne: Your Verification Partner

With 16 years of expertise in the digital realm, SquareOne empowers organisations with tech solutions to level up their services and performance. Understanding the crucial necessity of customer due diligence, SquareOne offers identity verification, customer onboarding, remote document examination, and anything related to forensic and identity verification, partnering with Regula. Its robust and intelligence-led verification framework helps organisations remain risk-ready, fraud-resilient, and fully compliant in a fast-evolving regulatory landscape.

Conclusion

Customer Due Diligence is a paramount process for financial institutions as it helps organisations to understand their customers and their risk profile. It mitigates any form of fraudulent activities that include Identity fraud, synthetic identity fraud, money laundering, mule account fraud, account takeover, document forgery, shell company fraud, and sanctions or PEP evasion. With crucial steps in CDD, like identity verification, financial institutions successfully evade fraud and focus on business growth and better performance.